Survey on AI Usage in Southeast Asia

Survey on AI Usage in Southeast Asia

Artificial intelligence is moving from experiment to everyday business use. Across industries, companies are testing AI tools to improve productivity, strengthen decision-making, automate routine work and find new sources of competitive advantage. For small and medium-sized enterprises, the question is no longer whether AI will affect their business, but how quickly they can automate AI into useful, reliable and measurable results.

Voyager AI conducted this survey for the Cañizares Center for Emerging Markets (EMC²) at Cornell University to better understand how businesses are approaching AI adoption in practice. The results capture a region moving quickly from curiosity to applied use, while still working through the operational realities that determine whether AI creates lasting value: skills, governance, data readiness, workflow integration, privacy, reliability and return on investment.

This survey catches the work in progress as a snapshot of how companies are using AI today, where adoption is gaining momentum, and where firms remain cautious. AI is already being applied and respondents discuss the barriers they face in implementation, and the opportunities they see for improving efficiency, growth and competitiveness.

For Voyager AI, these findings reflect the same pattern we see in our work with businesses:

AI adoption succeeds when it is tied to real workflows, precise data, clear governance,

and measurable business outcomes.

Through this initiative, Voyager AI aims to share practical insight and best practices with EMC² and help companies move beyond experimentation toward responsible, secure and productive AI adoption.

Respondents

Respondents

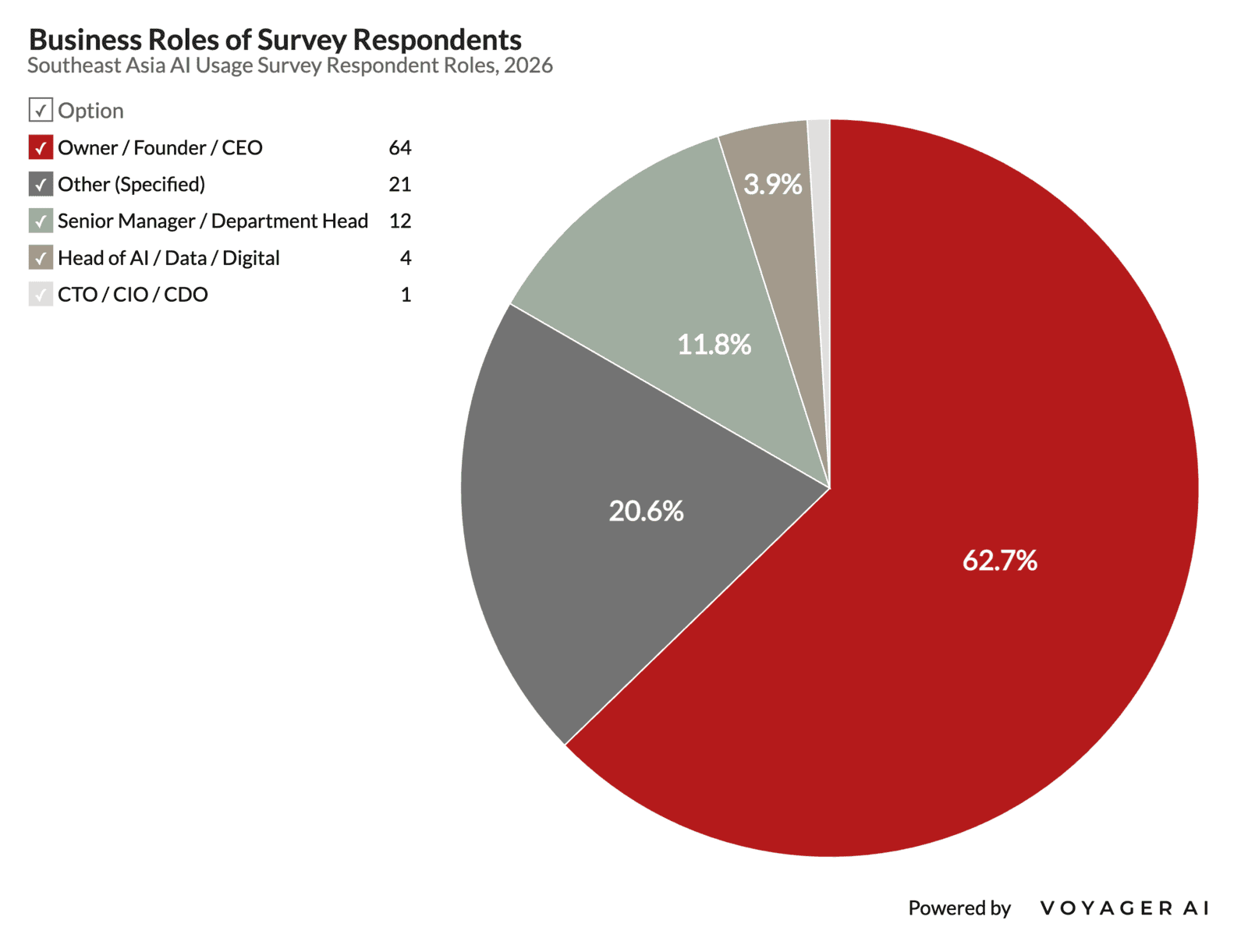

The survey was sent to more than 5000 businesses in Southeast Asia with completions making up 102 responses. It did not target quantitative coverage of the region, but qualitative familiarity with the firms making adoption decisions. The sample is business-led: 63% of respondents are owners, founders or CEOs.

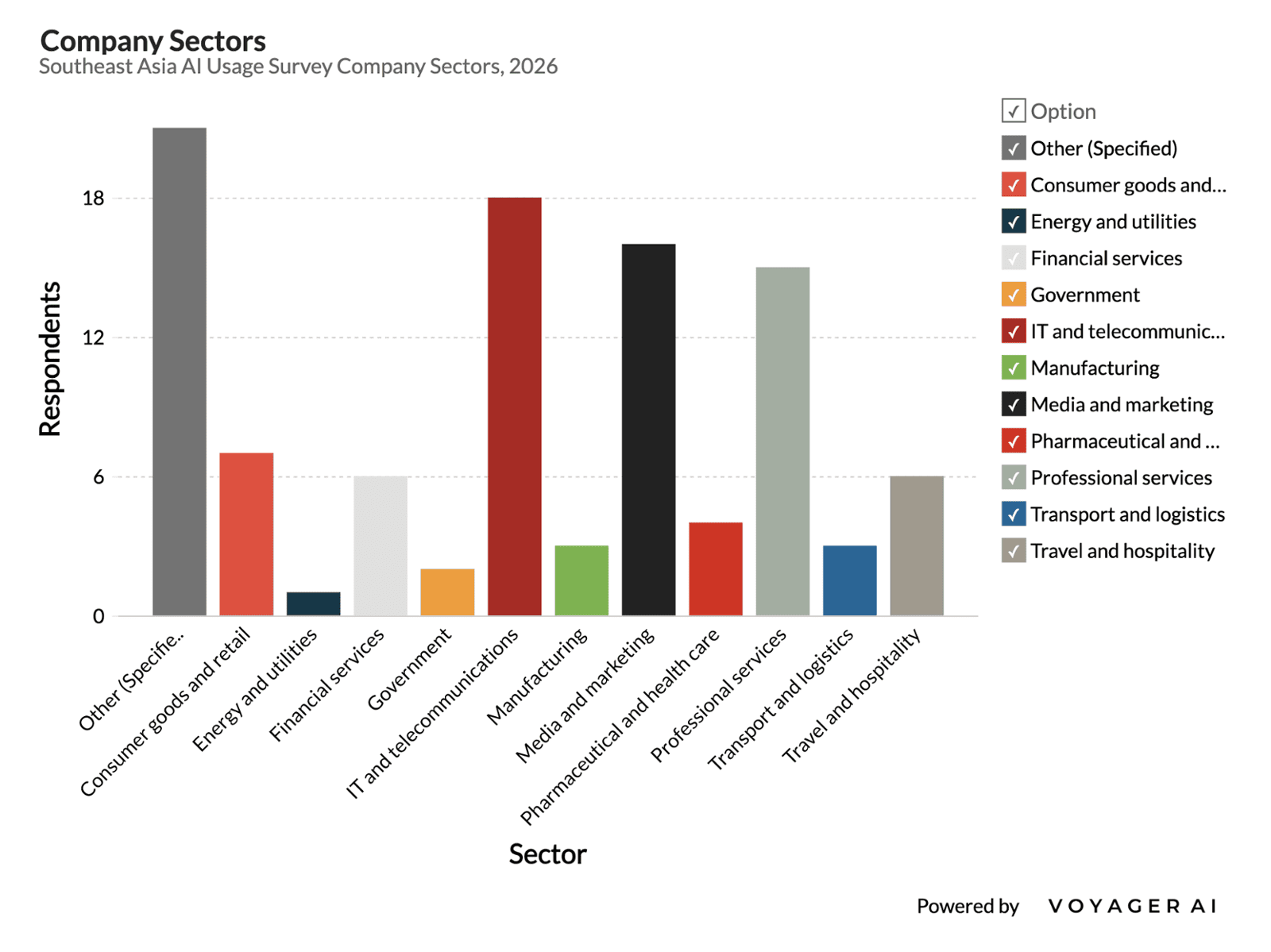

While respondents leaned heavily towards business owner and executives, the sectors that responded were exceptionally broad. In addition to the ones listed in the chart, replies were also received from Education (4), Real Estate (4), Wellness, Luxury Goods, Gaming, Executive Search and Trade sectors.

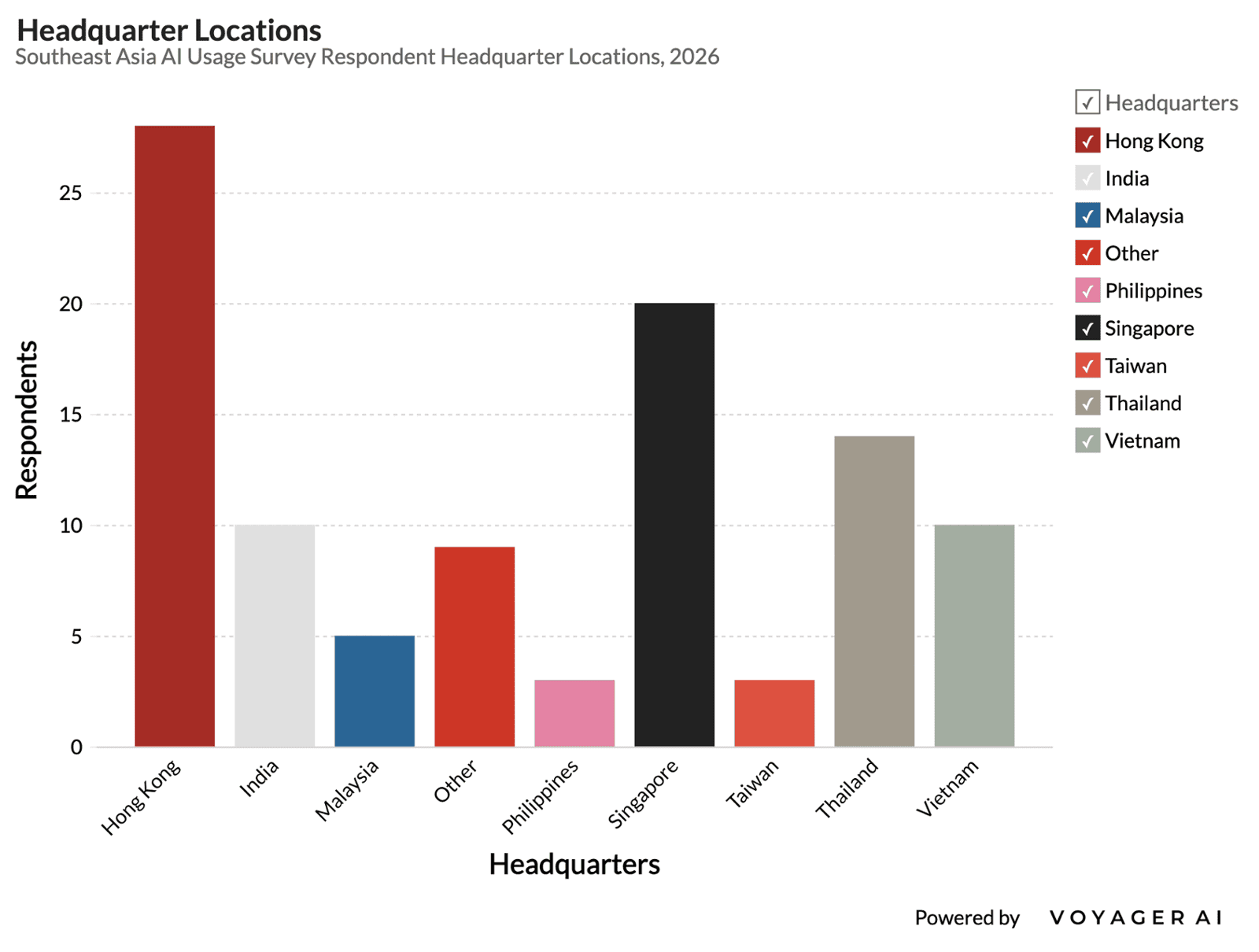

Respondents were contacted based on business activity in Southeast Asia. Their headquarters were likewise often located in the region, or adjacent. The "Other" category is made up of: USA (3), China (2) and the UK, Australia, Japan, and Italy at one each. The mix of responses from Hong Kong, Singapore, Thailand, Vietnam, Malaysia, Philippines, Taiwan, and India provide on-the-ground insights into how AI is being adopted in the region.

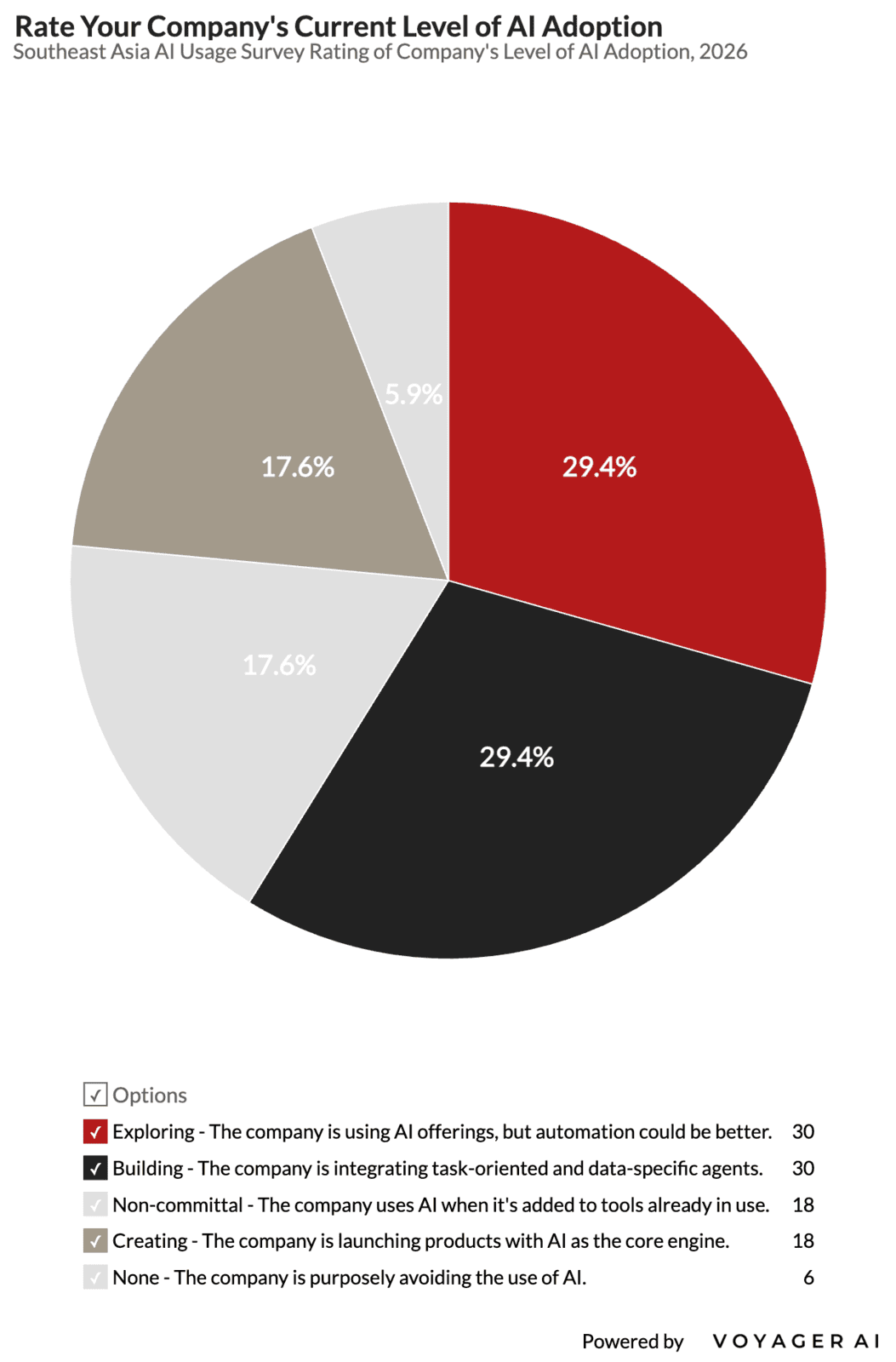

Company AI Adoption

Company AI Adoption

The survey shows that Southeast Asian businesses have largely accepted AI’s relevance, with this section measuring how far along businesses are with adoption.

One Hong Kong respondent described the shift from tool interest to organizational change by noting that:

“AI adoption is seen as a cultural evolution,

not a technical race.”

While a Singapore respondent put the same point in commercial terms: “Budget allocation flows toward use cases with quantifiable business impact, not technology for its own sake.”

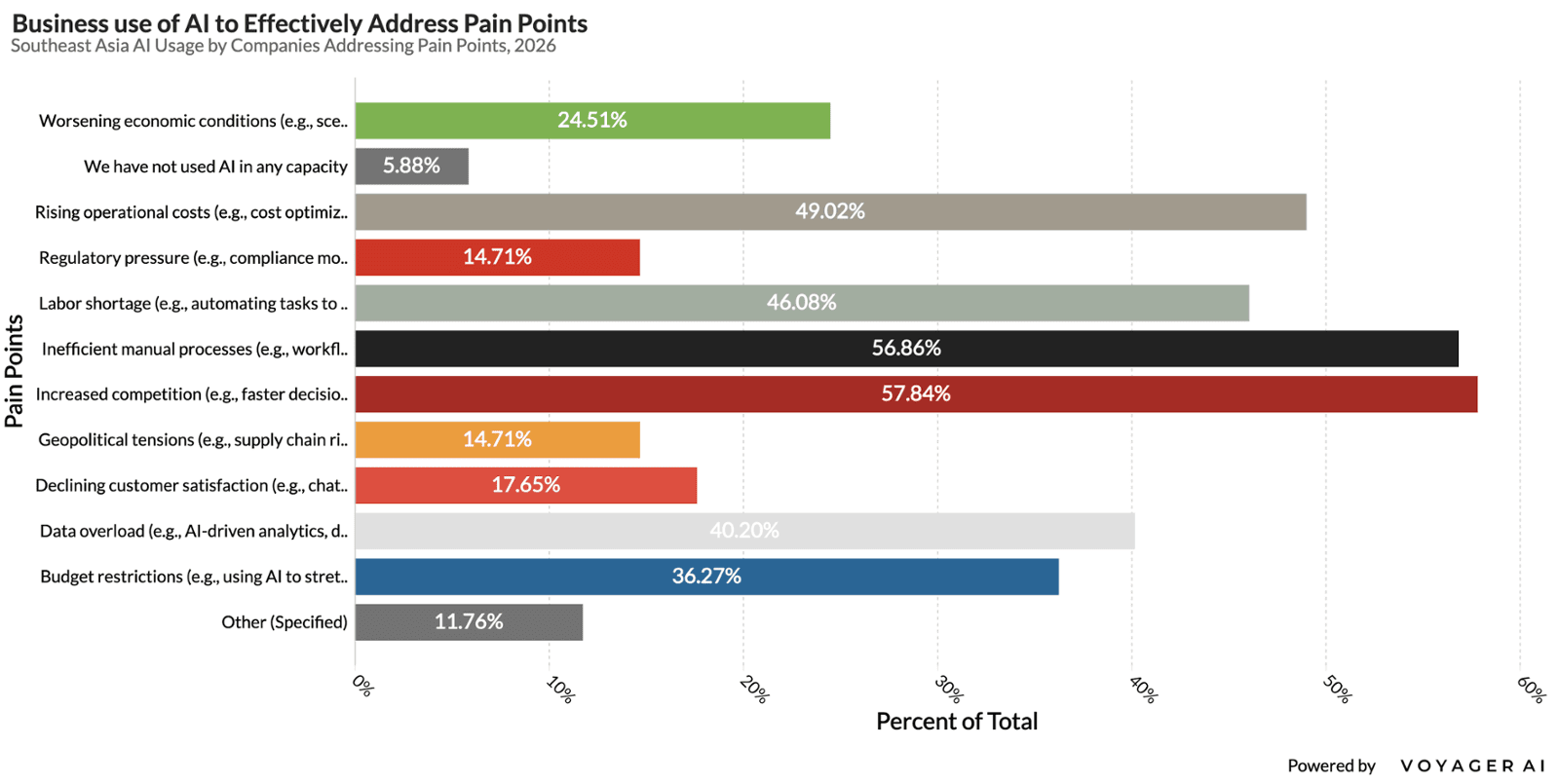

A majority of businesses in Southeast Asia are tasking AI with practical uses, as more than half of respondents say they use AI to address increased competition and inefficient manual processes. Near the 50/50 margin, business are working to cut rising operational costs and labor shortages. Many other uses were cited as outlined in the next chart.

For other pain points, respondents cited using AI for general enabling technology, avoiding unnecessary outsourced costs, budgeting, marketing, BD, expedition requests, exploration of pivots, studies, strategic analysis & assessment, business planning, and even the creation of new products and offerings. These pressures all make Southeast Asia a promising adoption region as they address competitive markets, lean teams, high service expectations and persistent administrative bottlenecks.

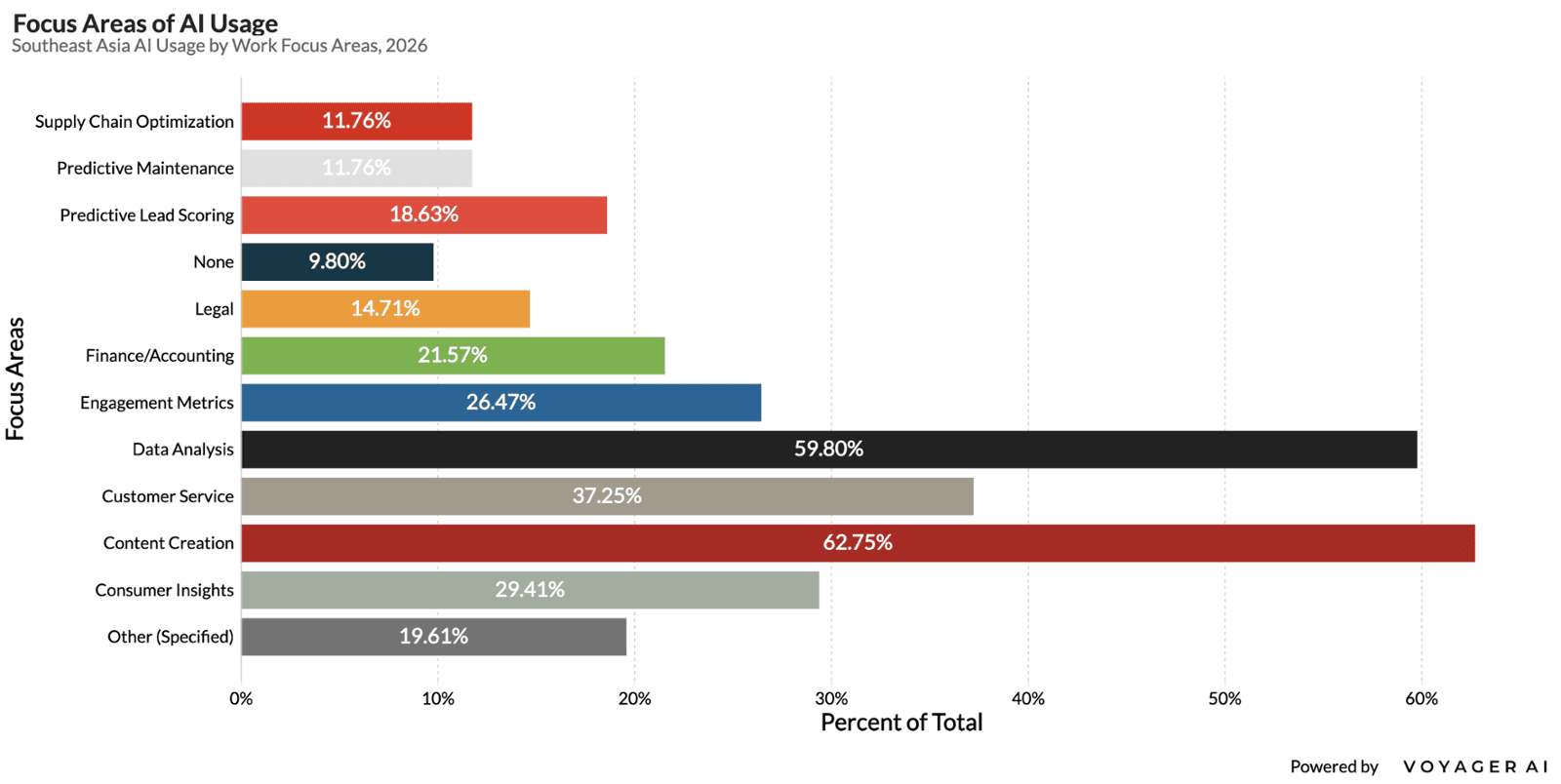

Content creation and data analysis lead AI uses in work focus areas by a wide margin (~60%), while a third (26-37%) of businesses are tasking AI with customer facing tasks, such as service, insights, and engagement. Areas that have been slower to be addressed are Finance and Accounting (22%), Predictive Lead Scoring (19%), Legal (15%), Predictive Maintenance (12%), and Supply Chain Optimization (12%). General enablement uses make up other use cases specified by respondents: software development, research, troubleshooting, website performance auditing, and classroom engagement.

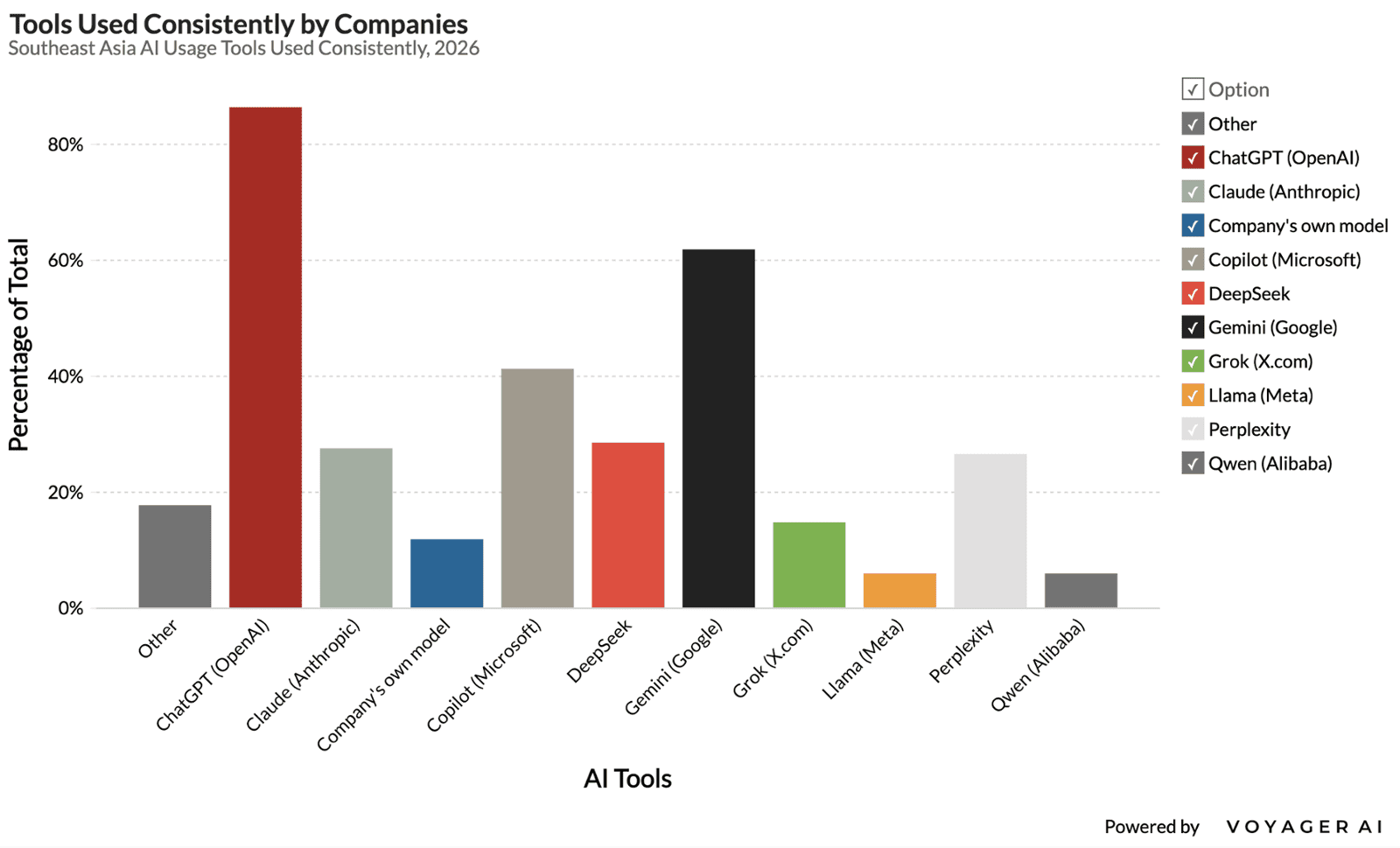

ChatGPT gained substantial and exposure in the region and still leads while Google Gemini has been quick to make up ground. Copilot frequently appears within model usage reports due to many enterprise systems relying on the Microsoft OS. Unlike Western markets though, Southeast Asia also employs China-developed models such as DeepSeek and Qwen. Claude and Perplexity are near DeepSeek in usage while company's developing their own models or open source configurations are slightly less common than Grok use and more popular than Llama.

Of the respondents who marked Other, pre-packaged AI tool usage included: Earlybird, Midjourney, Canva, Beautiful.ai, Librechat, Freepik/Magnific and Google NotebookLM from approximately half of the responses. The other half described workflow automation and software development tools from creating new products with AI as the core engine to development pathways such as, Cursor, n8n, Make, and MCP Frameworks. From this group, a reply from Hong Kong further captured their ethos:

“An agentic AI bot has been a game changer for us... quality output in a fraction of the time.”

This group also cited the need for protecting data and working with local AI that could interact with that data within their own network. As more of Southeast Asia engages with AI in automations at the workflow level, the trend towards more localized and embedded systems will likely continue.

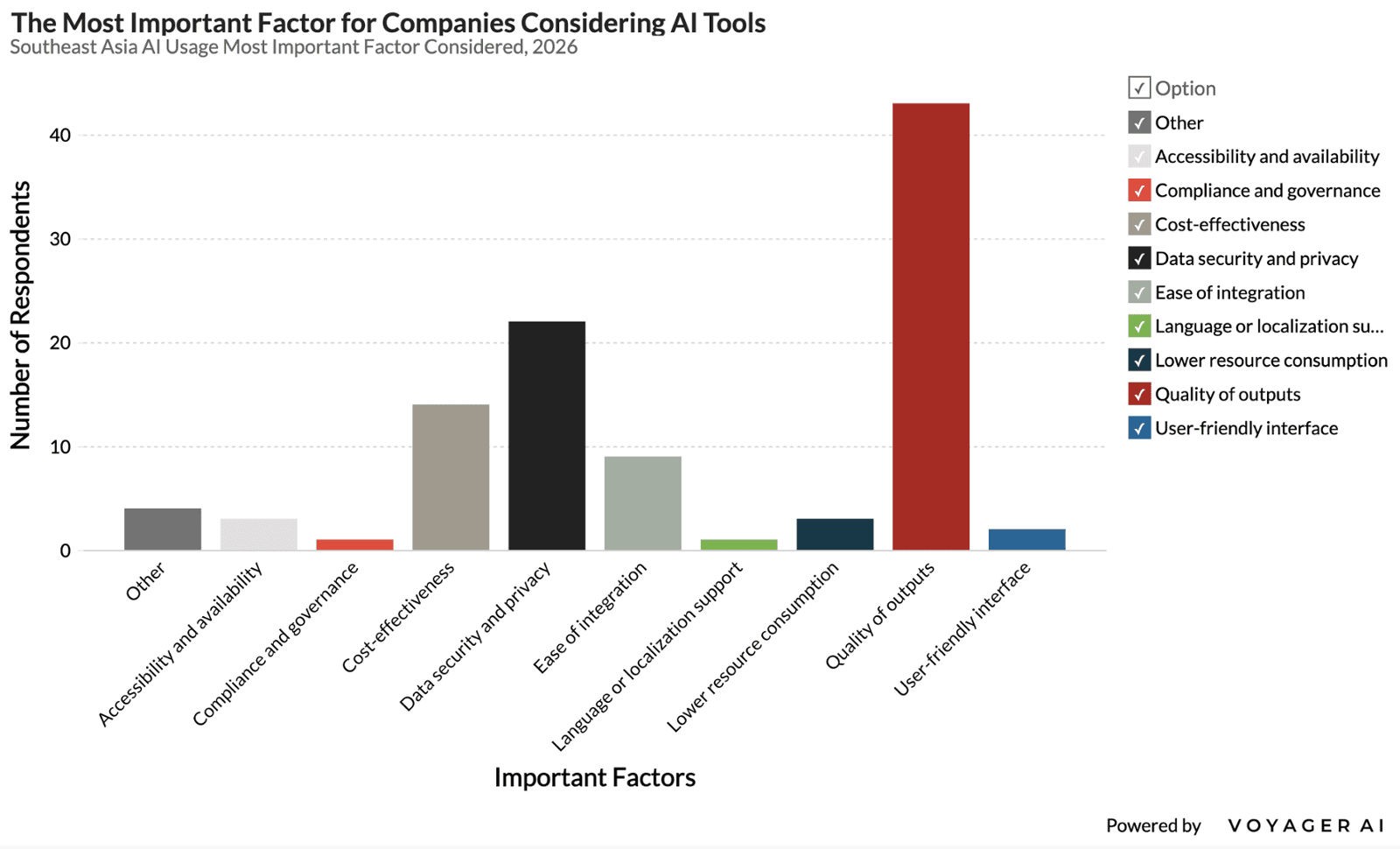

The quality of AI outputs is a consistent primary factor for businesses working with and working to embed AI, approximately doubling the next highest consideration: Data security and privacy. Together, both demonstrate the trend towards adoption and making investments in AI produce positive returns. Cost-effectiveness and Ease of integration were the two other significant considerations.

Company AI Challenges

Company AI Challenges

What challenges will your company face, or have faced, in adopting usage of AI?

Survey respondents framed AI adoption as an execution challenge rather than a lack of interest. The main barriers were data readiness, fragmented systems, budget, integration costs, staff training, cultural resistance, privacy, governance, and output reliability. Many companies are still moving from experimentation to production, with one respondent noting that “each team has their own needs” but no shared company-level tool for consolidation. Human resistance also appeared frequently, including fears that “people will be replaced” and frustration that staff “don’t want to learn new things/skills.” Trust remains a major constraint: respondents cited “AI hallucinations,” unreliable outputs, “client trust and confidentiality,” and concerns that confidential data could be used for model training. Yet the responses were not uniformly negative. Some companies reported “no challenges” or “smooth integration so far,” while smaller firms saw agility as an advantage. Taken together, the results suggest that AI adoption is advancing, but value depends on moving beyond ad hoc tool use toward secure, reliable, well-governed workflows.

With or without AI, what processes have been the most stubbornly inefficient, time-consuming, or driven the most pain points within your company?

Respondents identified the most stubborn inefficiencies in the routine but critical work that holds organizations together: administration, reporting, approvals, data consolidation, customer service, sales follow-up, content creation, client coordination, and knowledge management. Many cited fragmented systems and manual handoffs, including “manual data consolidation and reporting across departments,” “manual handoffs between sales, delivery, and ops,” and “knowledge fragmentation across tools, documents, and teams.” Sales and growth remain especially painful, with respondents naming “lead generation and sales,” “prospect client outreach,” and “lead engagement and the sales cycle.” Administrative burdens also persist, from “billing, invoicing, taxes” and “accounting reconciliation” to internal reporting and meeting follow-up. AI is already improving some repeatable work, especially “content creation, proposal writing” and customer service, but respondents were clear that technology alone does not fix broken processes. One noted that meaningful improvement requires “breaking the old process flow,” which can create resistance when roles and responsibilities are affected. Taken together, the responses suggest that AI’s greatest value may come not from automating isolated tasks, but from redesigning workflows across data, people, systems, and decisions.

How do you evaluate AI service vendors in Asia?

Respondents varied widely in how they evaluate AI service vendors in Asia. More mature buyers use structured criteria: technical capability, domain expertise, security, compliance, scalability, localization, pricing transparency, integration, and long-term support. One respondent prioritized “production experience over demos or prototypes,” while another called “data security, privacy compliance, and governance standards” “non-negotiable.” Regulated organizations were especially strict, with one noting that failure on compliance “disqualifies a vendor immediately,” and others requiring data localization, explainability, bias mitigation, security audits, and local support. Many smaller firms, however, had no formal process, citing “no set benchmarks,” “no real evaluation metric,” or relying on “word of mouth and self-validation.” Practical factors such as “output, prompt adherence, speed and security,”“cost and quality,” and “ease of usability, price” often mattered most. The responses also show mixed confidence in the regional vendor market. Some respondents saw Asian vendors as “fast growing and ambitious,” with strengths in local language and cultural understanding, while others said there are “no trustworthy and productive players yet” or that “the best companies are in SF.” Overall, vendor evaluation in Asia appears disparate: rigorous among larger or regulated organizations, but still informal, experimental, and trust-driven among many smaller businesses.

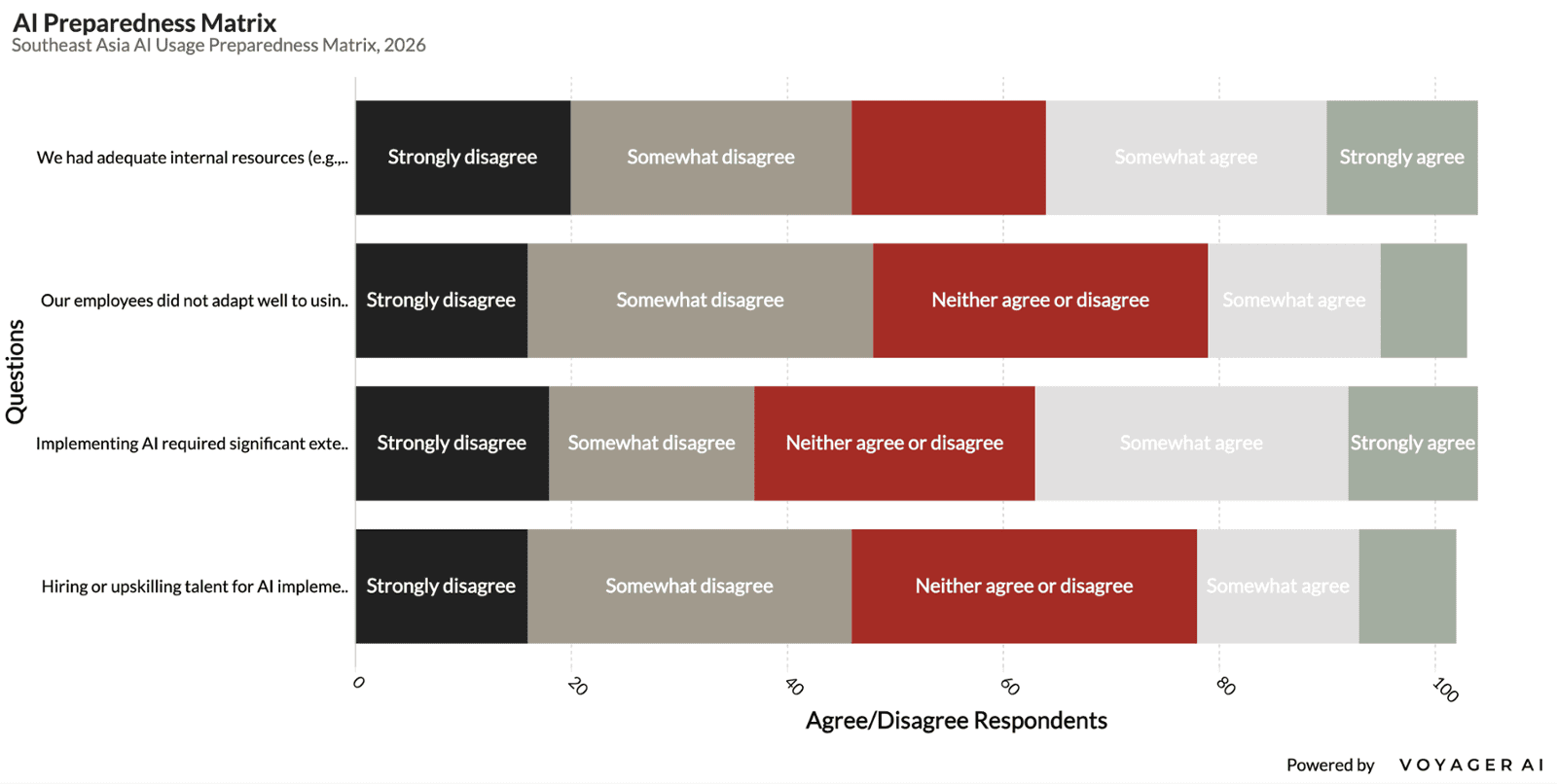

| Questions | Strongly disagree | Somewhat disagree | Neither agree or disagree | Somewhat agree | Strongly agree |

| We had adequate internal resources (e.g., data scientists, engineers, project managers) to support AI adoption | 9.61% (20) | 25.49% (26) | 17.65% (18) | 25.49% (26) | 13.73% (14) |

| Hiring or upskilling talent for AI implementation was easy | 15.69% (16) | 29.41% (30) | 31.37% (31) | 14.71% (15) | 8.82% (9) |

| Our employees did not adapt well to using AI tools in their daily work | 15.69% (16) | 31.37% (32) | 30.39% (31) | 15.69% (16) | 7.84% (8) |

| Implementing AI required significant external support or consulting services | 17.65% (18) | 18.63% (19) | 25.49% (26) | 28.43% (29) | 11.76% (12) |

The AI preparedness matrix suggests that companies are not starting from zero, but few feel fully equipped to adopt AI at scale. On internal resources, respondents were almost evenly divided: 39.22% agreed or strongly agreed that they had adequate internal capacity, while 35.10% disagreed or strongly disagreed. This points to a region where AI ambition often runs ahead of organizational depth.

The clearest weakness is talent development.

Only 23.53% agreed that hiring or upskilling AI talent was easy, compared with 45.10% who disagreed, while the largest single group remained neutral, suggesting uncertainty or mixed experiences across firms. Employee adaptation appears less negative than expected: 47.06% disagreed that employees failed to adapt well, while only 23.53% agreed, implying that staff resistance may be real but not the dominant barrier. The larger issue is capability-building around them. The strongest signal is the need for outside help: 40.19% agreed that AI implementation required significant external support or consulting services, against 36.28% who disagreed.

Taken together, the data show a market in transition. Many companies have willing employees and some internal capability, but AI readiness remains constrained by scarce technical talent, limited resourcing, and the need for external partners to convert experimentation into repeatable business value.

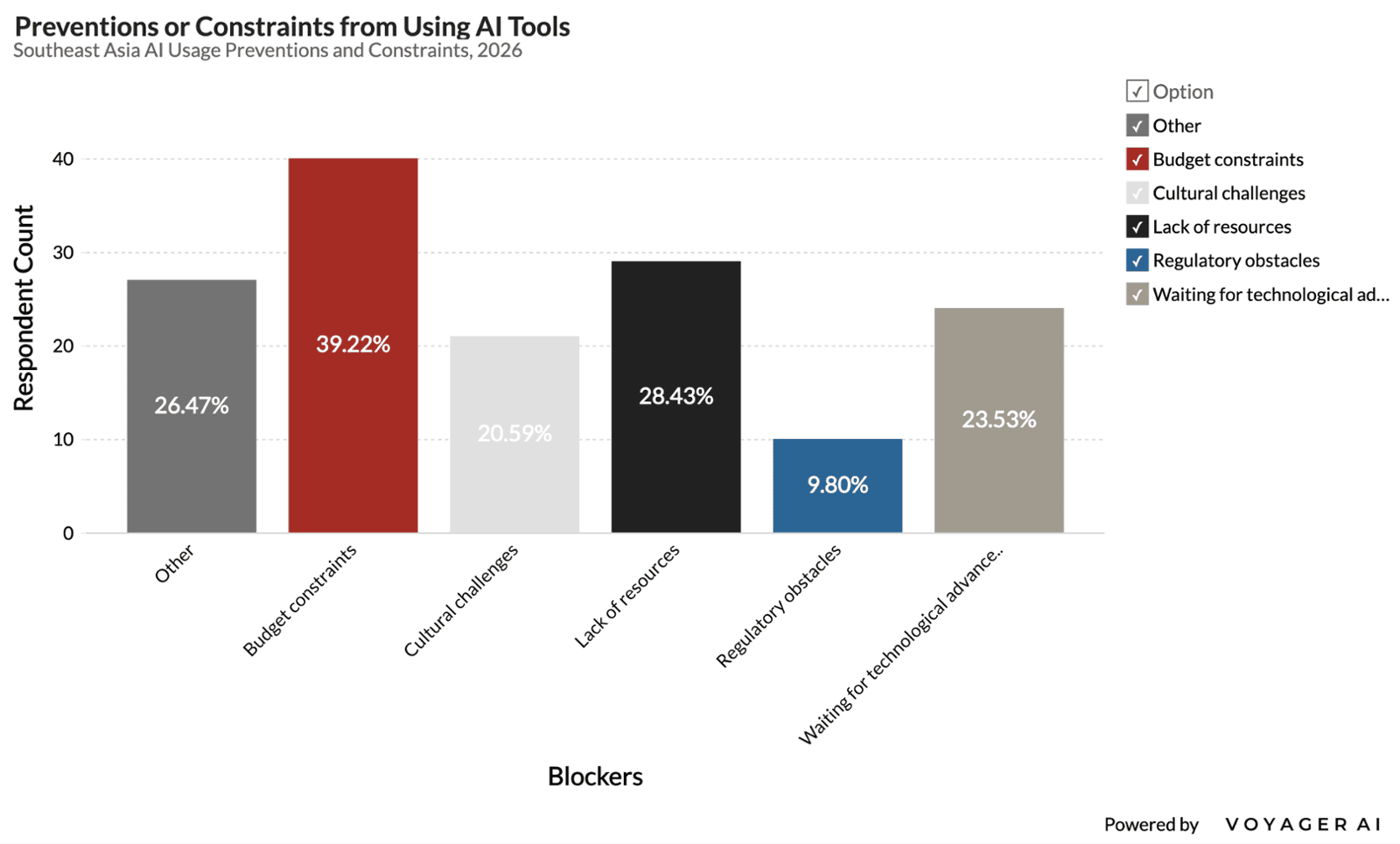

Among respondents who face constraints in using AI tools, the leading barrier was budget. Nearly four in 10 respondents cited budget constraints, making cost the clearest practical obstacle to wider adoption. Lack of resources followed at 28.43%, suggesting that many companies do not yet have the staff, time, systems, or implementation capacity needed to use AI consistently. A notable 23.53% said they are waiting for technological advancement and cultural challenges were also significant at 20.59%, while regulatory obstacles were less common, cited by 9.80%, but still important for more sensitive or compliance-heavy organizations. The open-ended responses add useful texture: several respondents pointed to “lack of know how,” “lack of sufficient training,” “quality inconsistency,” legal review, token limits, and uncertainty about the right “use case.”

At the same time, many “other” responses came from companies already using AI, suggesting that the constraint question captured both nonusers and active users who still experience friction. Overall, the data show that the main barriers are not rejection of AI, but the practical difficulty of making AI affordable, reliable, well understood, and easy to integrate into daily work.

Infrastructure and Data Readiness

Infrastructure and Data Readiness

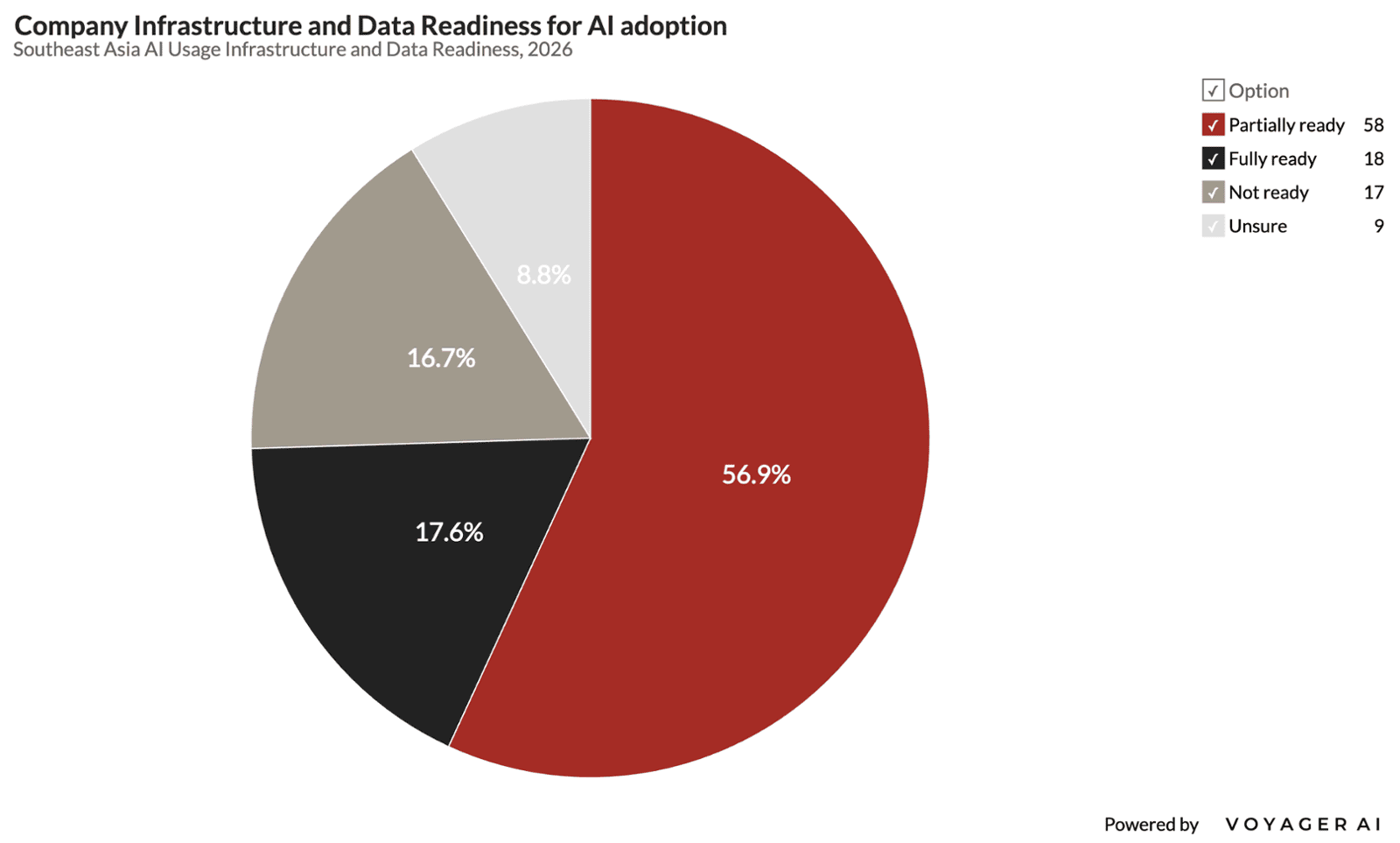

Infrastructure and data readiness are emerging as decisive constraints on AI adoption in Southeast Asia. While 17.65% of respondents said their companies are fully ready, the much larger share, 56.86%, described themselves as only partially ready. This suggests that many firms have begun building the foundations for AI, but still face gaps. A further 16.67% said they are not ready, and 8.82% were unsure, underscoring how divergent preparedness remains across the region.

The result is a picture of strong momentum but incomplete foundations: Southeast Asian companies are interested in AI, but many still need cleaner data, stronger infrastructure, clearer ownership, and better-connected systems before AI can move from experimentation to scalable business value.

What type of data does your company keep and what do you do with it?

Respondents reported keeping a wide range of business, customer, operational, financial, employee, and project data, but the level of structure and sophistication varies sharply. Many companies use data for practical operating needs: customer follow-up, deliveries, sales tracking, marketing campaigns, accounting, reporting, compliance, and project delivery. Others described more advanced uses, including customer analytics, forecasting, campaign optimization, machine learning, internal knowledge management, and AI model training.

Common data categories included customer and client information, sales and transaction data, employee and HR records, financial and tax data, marketing performance data, website analytics, project files, product drawings, medical or student records, and audit or access logs. Several respondents emphasized confidentiality, noting that data is “not to be shared,” “confidential,” or handled only under NDAs, access controls, anonymization, deletion policies, or local privacy rules.

The answers also reveal a growing divide in data readiness. Some firms are building “master data” pools, using campaign data to “maximize ROI,” or aggregating data to improve forecasting and decision-making. Others keep data in basic tools such as OneDrive, Google Suite, email, CRM platforms, accounting software, or local storage, and admit that data is “utilised somewhat but not nearly to the extent it could be.”

Overall, the responses show that Southeast Asian companies hold valuable data assets, but many are still early in turning those assets into governed, integrated, AI-ready systems.

Risk Management and Governance

Risk Management and Governance

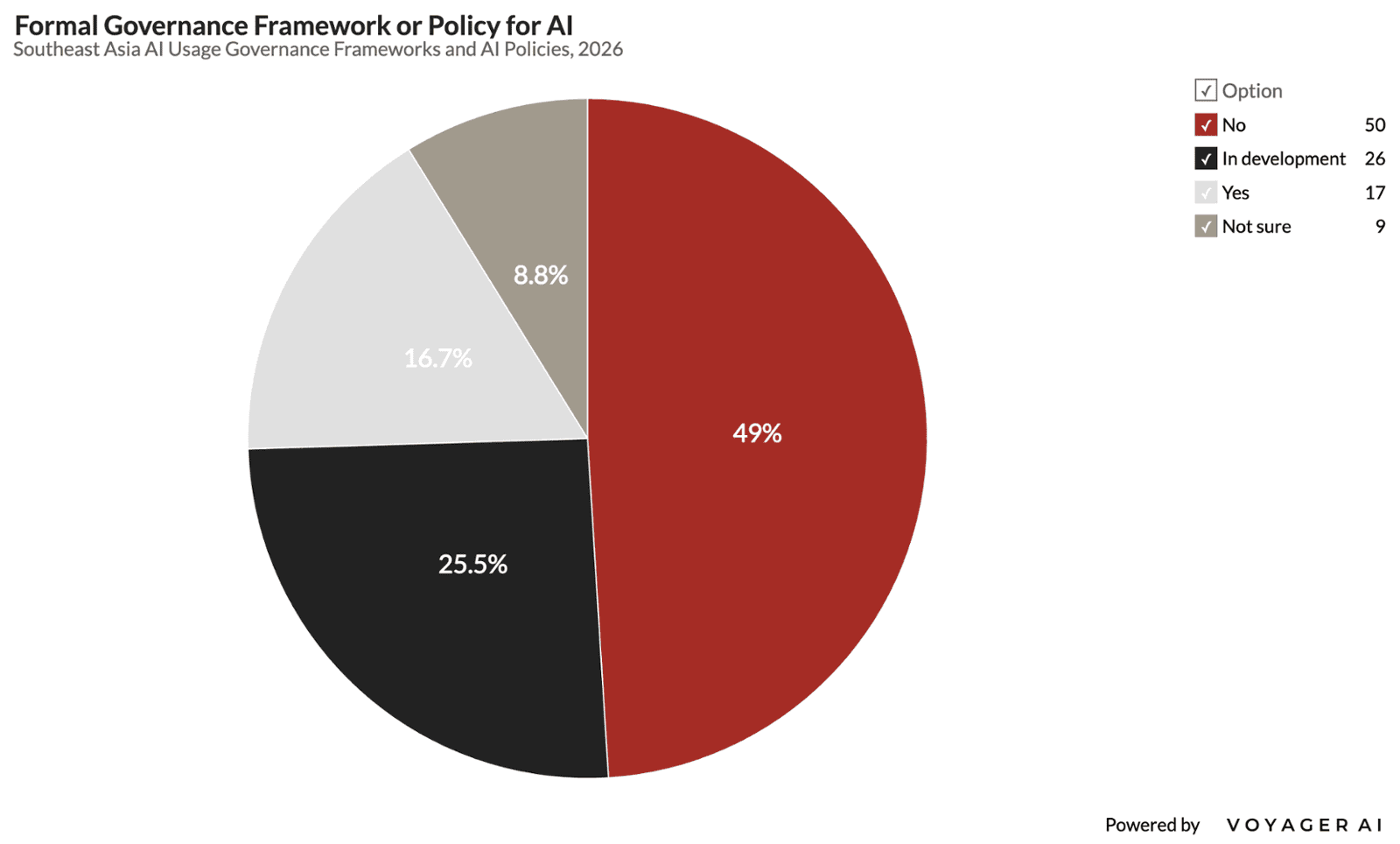

AI governance remains an early-stage capability for most respondents. Only 16.67% said their organization has a formal AI governance framework or policy in place, while nearly half, 49.02%, said they do not. Another 25.49% reported that a framework is in development, suggesting that many companies recognize the need for clearer rules but have not yet completed the transition from informal experimentation to managed adoption. The 8.82% who were unsure further indicates that AI policies, where they exist, may not yet be widely communicated across organizations.

Overall, the results point to a governance gap: AI use is advancing faster than the internal policies needed to guide security, accountability, data protection, employee use, and responsible deployment.

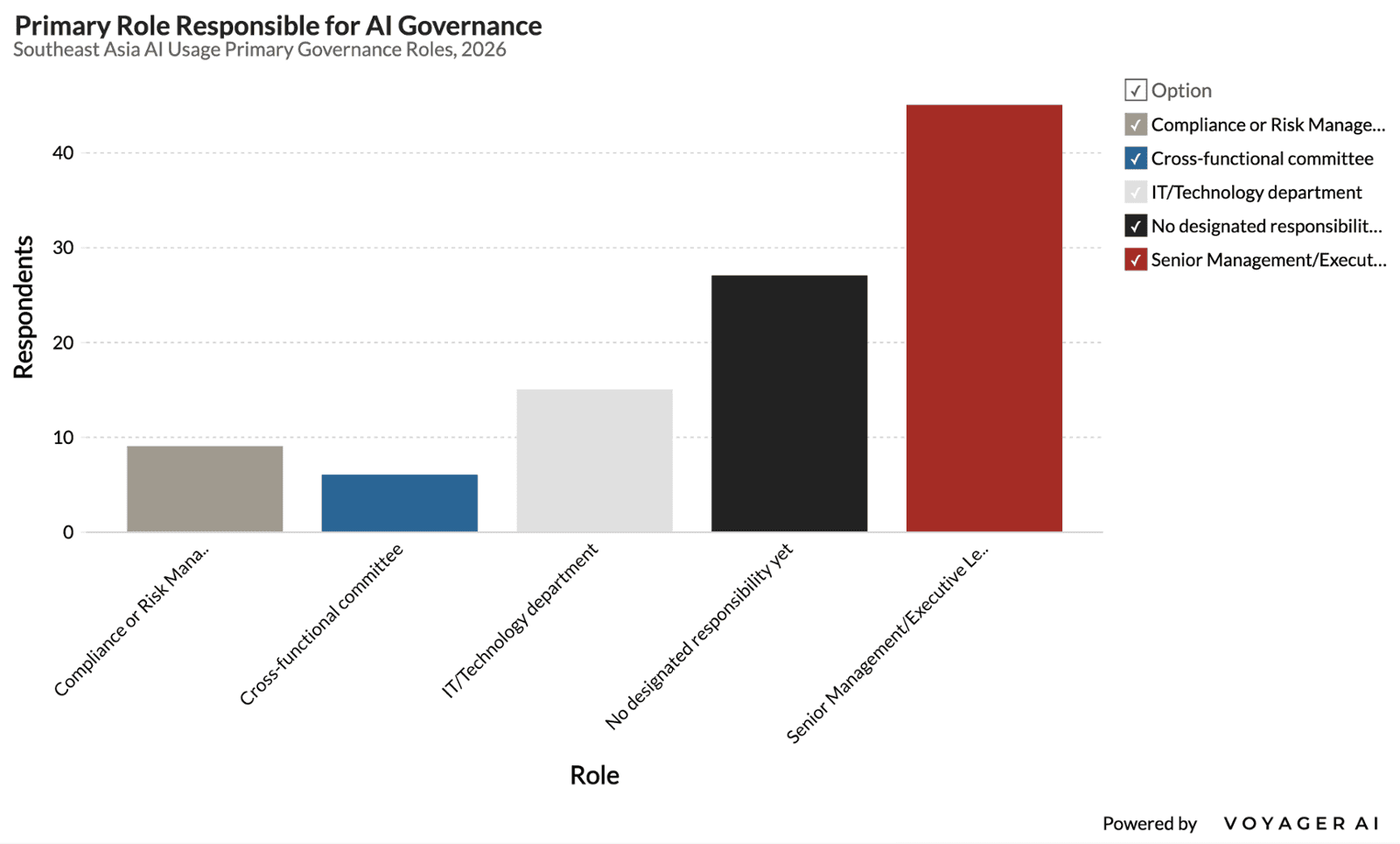

Responsibility for AI governance appears to sit mainly with leadership rather than specialized governance functions. The largest share of respondents, 44.12%, said senior management or executive leadership primarily oversees AI governance, suggesting that:

AI is increasingly viewed as a strategic business issue rather than only a technical one.

However, 26.47% said there is still no designated responsibility, exposing a significant accountability gap. Oversight by IT or technology teams accounted for 14.71%, while compliance or risk management teams represented only 8.82%, and cross-functional committees just 5.88%. This distribution suggests that many organizations have executive awareness of AI, but fewer have translated that awareness into mature governance structures involving technology, legal, risk, compliance, HR, and business units together.

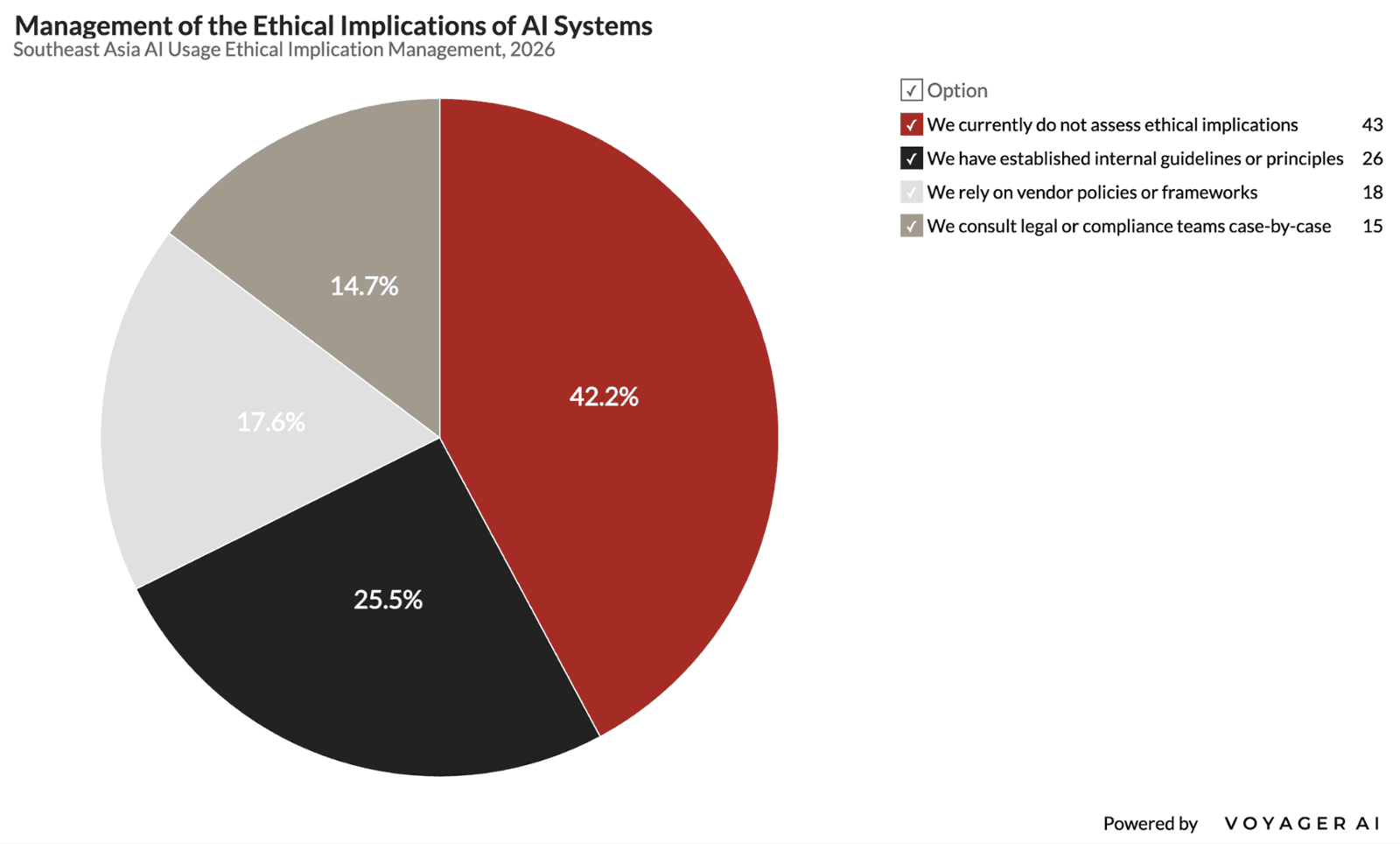

Ethical AI assessment remains one of the weakest areas of organizational readiness. The largest share of respondents, 42.16%, said their organization does not currently assess the ethical implications of AI systems, indicating that many companies are adopting or experimenting with AI prior to formal safeguards being in place. Only 25.49% reported having established internal guidelines or principles, while 17.65% rely on vendor policies or frameworks and 14.71% consult legal or compliance teams on a case-by-case basis. This suggests that ethical oversight is often reactive, outsourced, or informal rather than embedded into everyday AI use. As AI becomes more integrated, this gap may become more significant, particularly around bias, transparency, privacy, accountability, and trust.

What types of sensitive data does your AI system access (financial/health/behavioral etc.), and how do you secure it?

Respondents reported that AI systems, where used, may touch a wide range of sensitive data, including customer profiles, financial records, behavioral and marketing data, student and parent information, employee records, client project files, health or medical information, logistics data, CRM data, and campaign performance data. Financial and customer data appeared most frequently, while several education, healthcare, consulting, and marketing respondents described more sensitive use cases involving student records, patient diagnostics, borrower data, client financials, confidential strategy work, or retailer POS and loyalty data.

Security practices vary widely.

More mature respondents described layered protections such as encryption at rest and in transit, role-based access controls, anonymization or pseudonymization, secure APIs, private servers, vendor vetting, audit logs, compliance with PDPA, GDPR, HIPAA or local privacy rules, and private or on-premise AI environments.

Others avoid the uploading confidential information into public AI tools, filtering out PII before using public services, or using only enterprise versions of ChatGPT, Gemini, or other approved platforms. However, the answers also reveal wide range of readiness: some respondents said they were “not sure,” relied on existing software controls, or admitted that “all data is sensitive and we have not secured it.” Overall, the responses suggest that companies recognize the value of sensitive data for AI, but security maturity ranges from highly controlled governance frameworks to informal avoidance, redaction, and trust in third-party platforms.

Organization and Culture Challenges

Organization and Culture Challenges

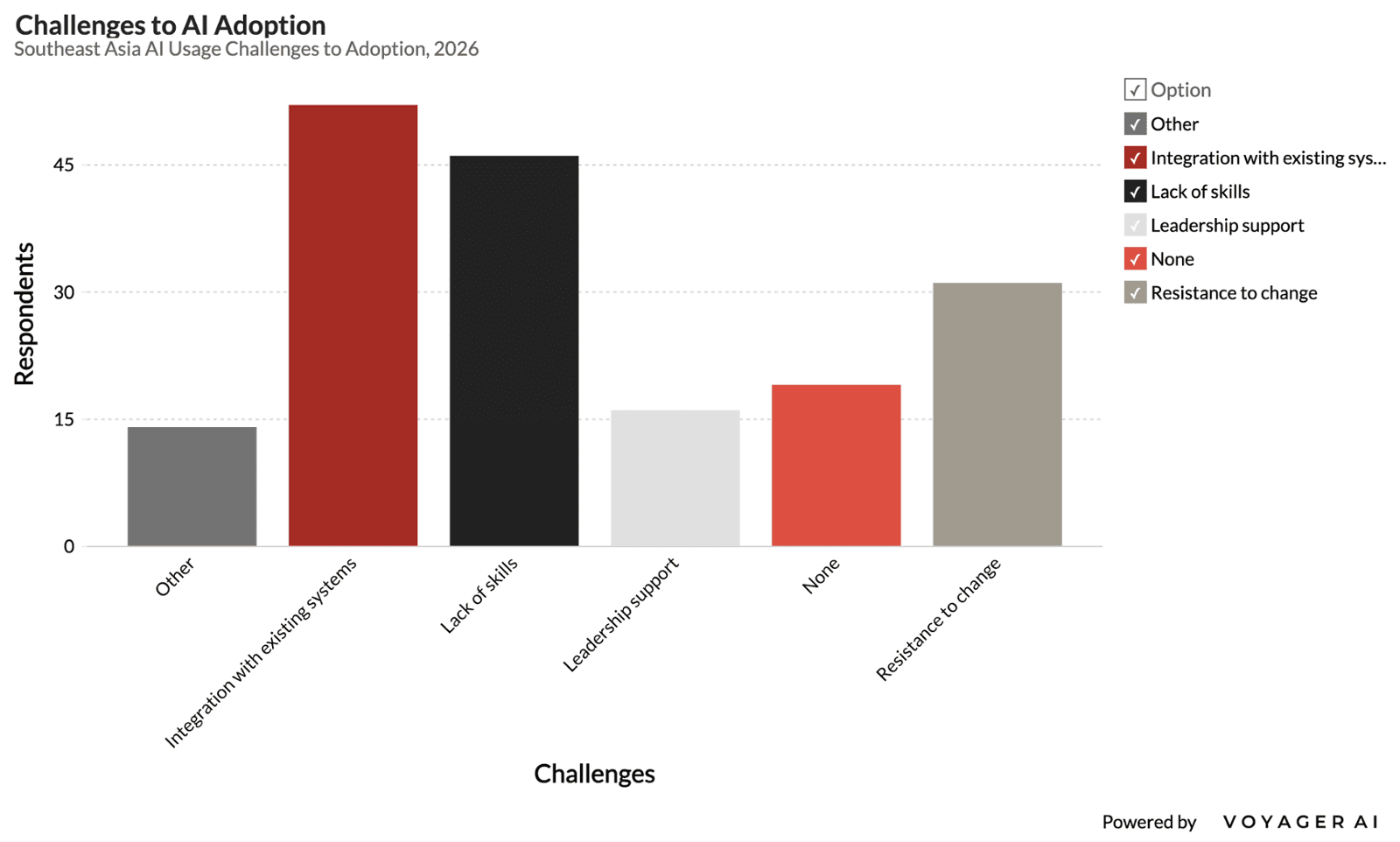

The survey shows that AI adoption is being slowed less by lack of interest than by the practical difficulty of fitting AI into existing organizations. The most common challenge was integration with existing systems, cited by 50.98% of respondents, followed closely by lack of skills at 45.10%. Resistance to change also remains material at 30.39%, while only 15.69% identified leadership support as a challenge, suggesting that many firms may have executive interest but lack the operational capacity to execute. Notably, 18.63% reported no major challenges, indicating that some organizations are already finding AI adoption manageable, especially where use cases are simple or narrow.

The open-ended responses add further nuance: respondents cited budgets, price, lack of dedicated AI process staff, output quality inconsistency, unclear processes, role conflicts, and the time required to keep up with new models. Overall, the results suggest that the next stage of AI adoption will depend on skills, integration, process design, and quality control more than enthusiasm alone.

How is your company currently addressing internal challenges?

Respondents are addressing internal AI challenges through a mix of structured transformation, informal experimentation, and gradual cultural change. More mature organizations described deliberate programs: centralizing data, modernizing legacy systems, building API-first integrations, creating governance processes, launching pilots with clear ROI metrics, forming task forces or AI working groups, and using external vendors where needed.

Training and upskilling were the most common responses, with companies citing staff education, government-funded courses, AI champions, mentoring, newsletters, creative labs, and “learning from doing” as ways to build confidence.

Several organizations are also taking a top-down approach, using executive mandates, KPIs, internal campaigns, and leadership encouragement to accelerate adoption. However, many responses show that internal change remains uneven.

Some companies are still “adapting as we go,” dealing with issues “one by one,” or have “no firm plan in place.” Others admitted they are “not effectively addressing” the problem, are waiting, procrastinating, or relying on traditional ways of working.

Overall, the answers suggest that companies are moving toward AI adoption pragmatically rather than uniformly: the leading firms are combining governance, training, integration, and pilot design, while many others remain in an exploratory phase shaped by limited resources, uncertainty, and ad hoc individual use.

Budget Trends and ROI Expectations

Budget Trends and ROI Expectations

Budgeting patterns suggest that AI remains an emerging investment category rather than a fully institutionalized business function.

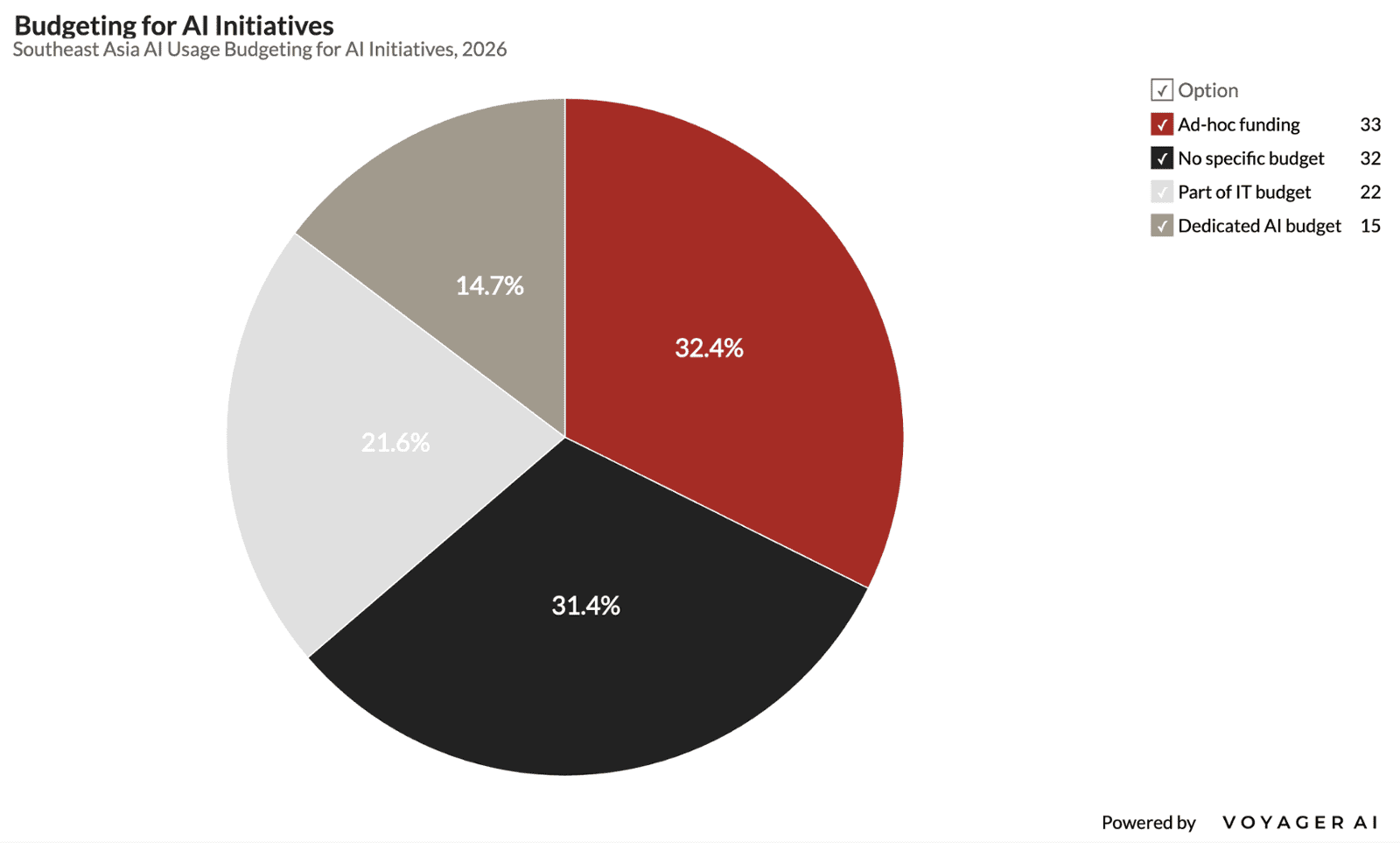

Only 14.71% of respondents reported having a dedicated AI budget, while 21.57% fund AI through the broader IT budget. The largest share, 32.35%, relies on ad hoc funding, and another 31.37% have no specific AI budget at all. This indicates that many companies are still experimenting, testing use cases, or absorbing AI costs into existing operations rather than treating AI as a planned strategic investment. As ROI expectations rise, the absence of clear budgets may become a constraint on scaling AI from individual productivity gains to enterprise-level transformation.

AI budgets are beginning to rise, but consistent investment remains spotty.

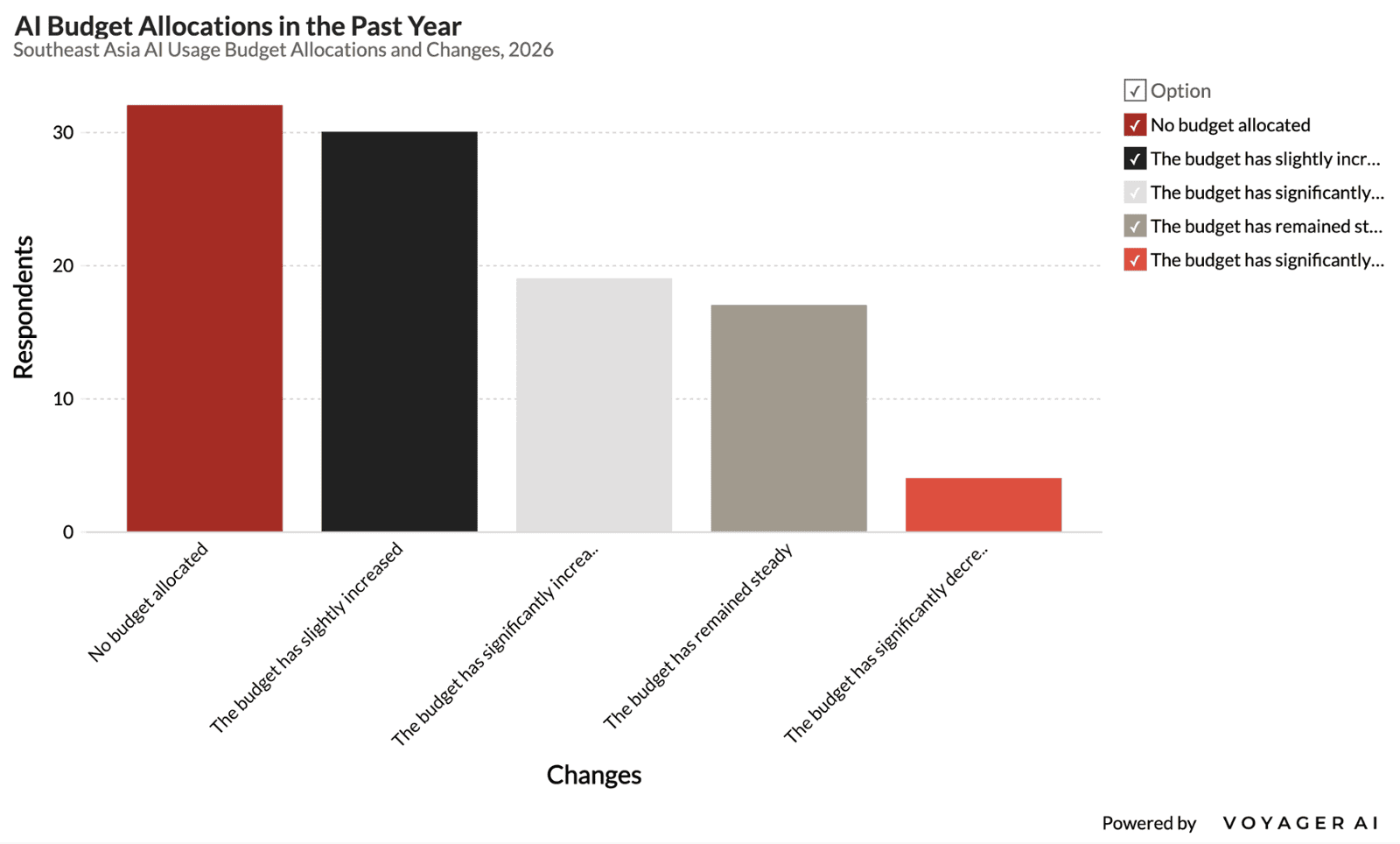

Nearly half of respondents reported some increase in AI spending over the past year, with 29.41% saying budgets slightly increased and 18.63% saying they significantly increased. This suggests that many companies are moving beyond casual experimentation and starting to allocate more resources to AI initiatives. However, 31.37% still reported having no AI budget at all, showing that a substantial share of organizations have not yet formalized AI as an investment priority. Another 16.67% said budgets remained steady, while only 3.92% reported a significant decrease and none reported a slight decrease. Overall, the pattern points to growing confidence in AI’s potential, but also a divided market: some companies are accelerating investment, while others remain at the starting line with no dedicated funding.

Looking ahead, AI budgets appear set to grow, but mostly in measured increments.

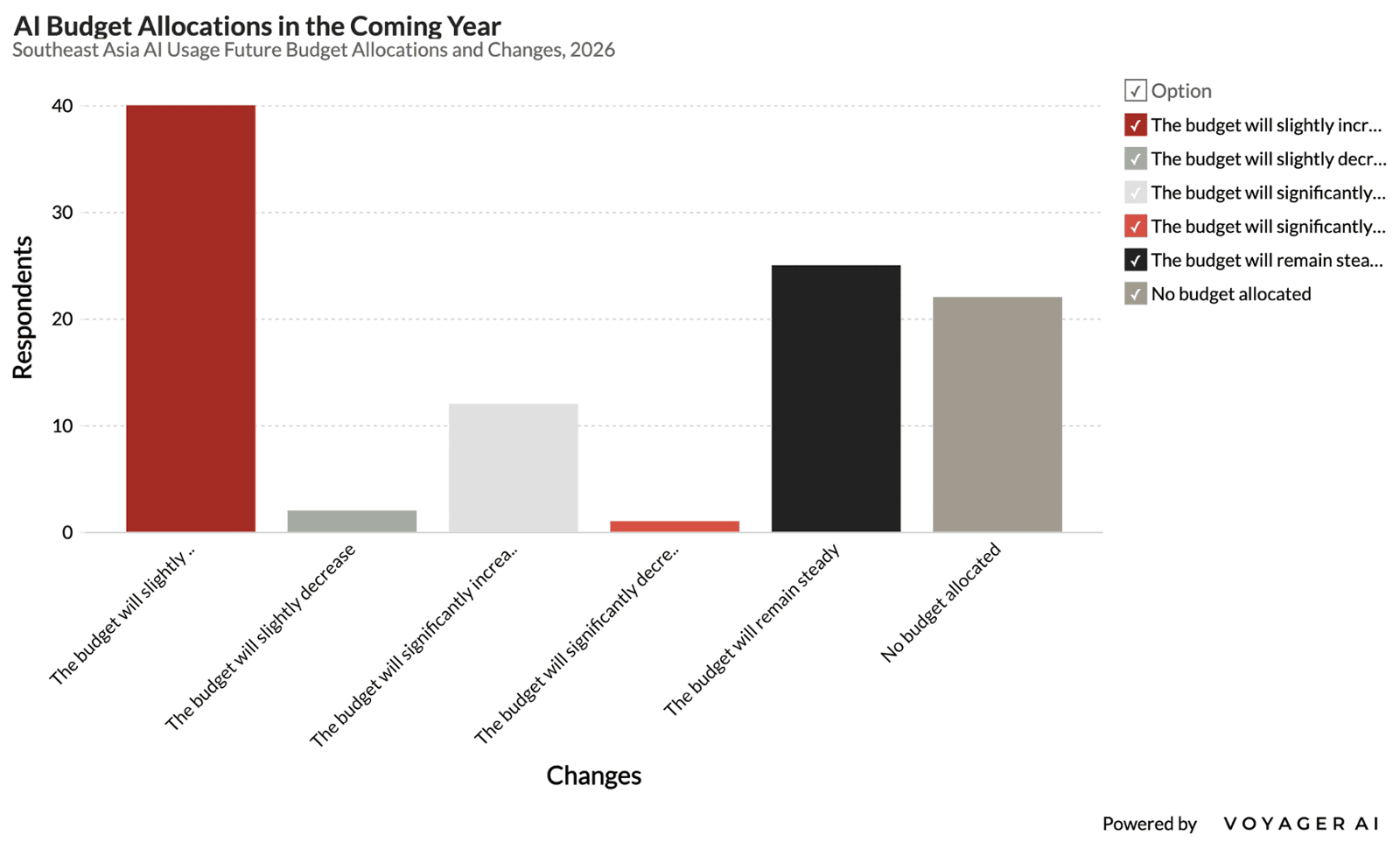

Just over half of respondents expect some increase in AI spending over the coming year, with 39.22% anticipating a slight increase and 11.76% expecting a significant increase. This suggests that many companies are becoming more confident in AI, but are still approaching investment cautiously rather than making large-scale commitments. Another 24.51% expect budgets to remain steady, indicating continued experimentation or maintenance of existing initiatives. The share with no AI budget falls to 21.57%, down from 31.37% in the previous-year budget question, suggesting that more companies may begin formalizing AI investment. Very few respondents expect reductions, with only 2.94% forecasting a slight or significant decrease.

Overall, the data point to a gradual shift from ad hoc adoption toward more intentional funding, though most companies remain careful about scaling spend until ROI, use cases, and implementation needs become clearer.

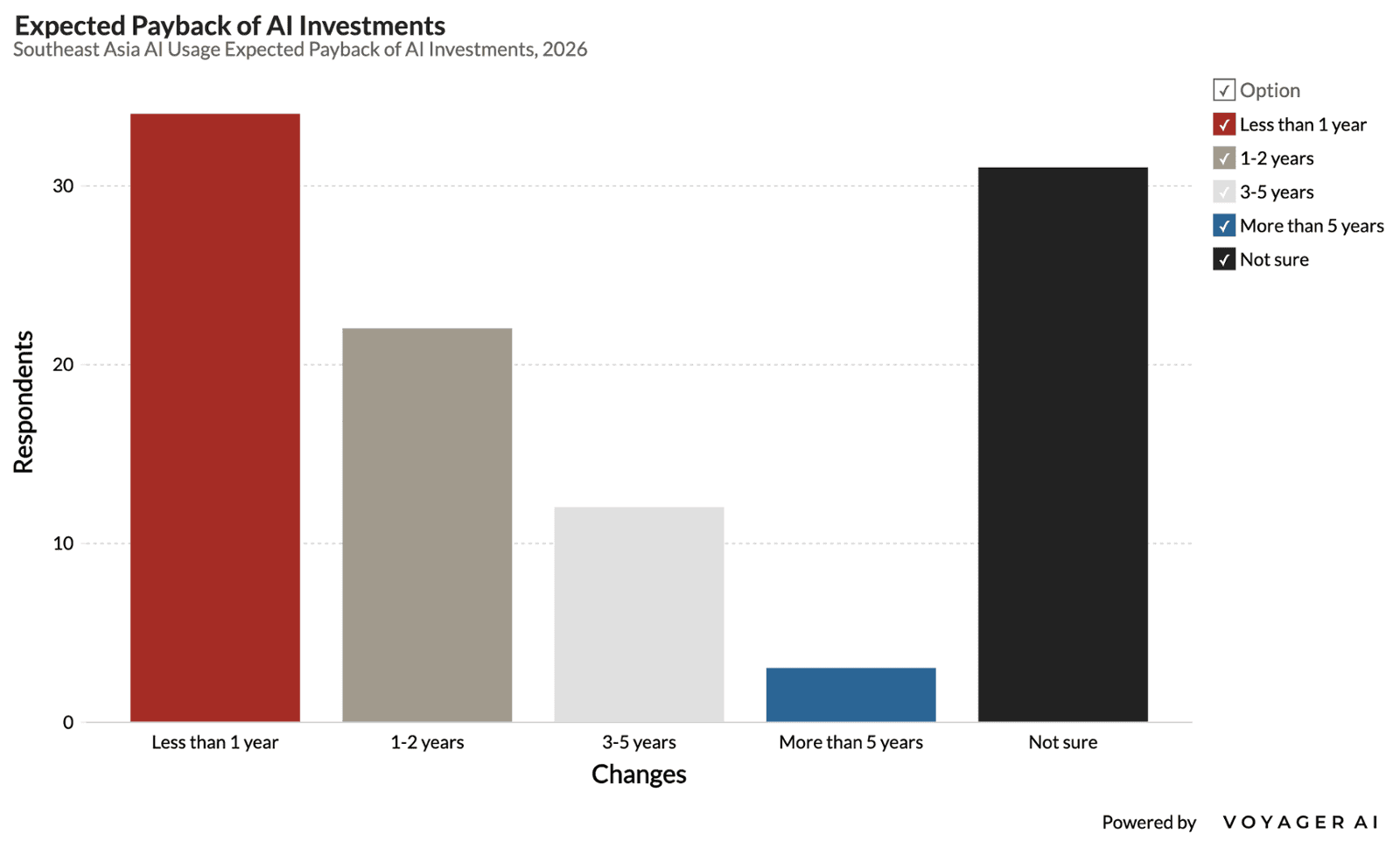

Respondents show relatively short payback expectations for AI investment, but with substantial uncertainty.

One-third expect AI initiatives to pay back in less than one year, while another 21.57% expect returns within one to two years. Taken together, more than half of respondents anticipate ROI within two years, suggesting that many companies view AI as a near-term productivity and efficiency tool rather than a long-horizon technology bet. A smaller share, 11.76%, expect payback over three to five years, and only 2.94% anticipate more than five years. However, 30.39% are not sure, underscoring the difficulty many organizations still face in measuring AI value, defining success metrics, and linking adoption to financial outcomes. Overall, the data suggest optimism about fast returns, but also a need for clearer ROI frameworks as AI spending becomes more formalized.

What factors would influence your budgeting decision for AI?

Respondents described AI budgeting as a practical business decision driven above all by ROI, cost savings, productivity, and clear use cases. The most common factor was whether AI can deliver measurable value: faster work, lower overhead, better output quality, revenue growth, improved customer service, or a clear payback period.

Many respondents said they would increase spending only if AI can prove a “direct impact on income or time saved,” reduce staffing or operational costs, or demonstrate “quick ROI.” At the same time, companies are cautious about hidden costs, including infrastructure, tokens, subscriptions, integration, training, vendor support, and long-term total cost of ownership.

Security, compliance, privacy, and data readiness also influence budgets, particularly for organizations handling sensitive or regulated data. Several respondents emphasized usability and adoption, noting that tools must be easy to implement, fit existing workflows, and not create an additional layer of work.

Others pointed to leadership buy-in, cash flow, government funding, team requests, competitive pressure, and the availability of better or more reliable tools.

Overall, the responses suggest that AI budgets will grow where companies can connect spending to specific business outcomes, but investment will remain cautious when use cases, ownership, output quality, or ROI are unclear.

Conclusion

Conclusion

The survey shows a region moving quickly into practical AI adoption, but not yet into mature AI transformation. Southeast Asian businesses are no longer treating AI as a distant technology or abstract trend. Most respondents are already exploring, building, or embedding AI into work, and expectations for increased usage are high. The strongest use cases remain practical: content creation, data analysis, customer service, research, reporting, process automation, and decision support. This reflects the region’s business reality. Many firms operate with lean teams, rising service expectations, competitive pressure, and stubborn manual processes. For these companies, AI is attractive because it promises faster work, lower costs, better use of data, and new ways to compete.

At the same time, the survey makes clear that AI adoption is not simply a matter of buying tools.

The biggest constraints are organizational. Companies face fragmented data, legacy systems, uneven infrastructure, limited AI skills, unclear ownership, budget pressure, governance gaps, and inconsistent output quality. Many respondents have valuable customer, operational, financial, marketing, health, education, and project data, but not all have the systems or policies needed to make that data secure, integrated, and AI-ready. Likewise, while senior leadership is often aware of AI’s importance, many organizations have not yet created formal governance frameworks, ethical review processes, cross-functional oversight, or clear rules for the use of sensitive information.

This gap between enthusiasm and readiness is a central finding of the survey.

Southeast Asia’s AI opportunity is full of potential, but the next phase will depend on execution discipline. Firms that benefit most will be those that move beyond ad hoc experimentation and connect AI to specific workflows, measurable ROI, reliable data, staff training, privacy safeguards, and business outcomes.

The survey also suggests that AI adoption may be especially powerful for SMEs, not because they have the deepest technology resources, but because they can be agile, pragmatic, and close to the operational problems AI can help solve.

The path forward is therefore not “AI everywhere” for its own sake. It is responsible, targeted adoption: choosing high-value use cases, protecting private data, improving internal capability, integrating AI into existing systems, and measuring whether the work becomes faster, better, safer, or more profitable.

In Southeast Asia, AI adoption is already under way. The companies that turn early use into durable advantage will be those that treat AI not as a novelty or shortcut, but as a disciplined business capability built around people, data, governance, and real work.